How much will insurance go up after a speeding ticket in Ontario? A speeding conviction can raise your car insurance by roughly 10% to 30% for most tickets, and the increase typically lasts three years — often far longer than the fine itself is remembered. In real dollars, a common 3-to-4 demerit-point conviction could add somewhere between $1,785 and $4,335 over three years. The exact amount depends on your insurer, your record, and the speed you were convicted at. The only way to fully avoid the increase is to avoid the conviction — which is why many drivers choose to fight the ticket rather than pay it.

How Much Does a Speeding Ticket Raise Insurance in Ontario?

Based on Ontario insurance industry data, here is roughly what a speeding conviction could cost you over three years, grouped by demerit-point classification. Treat these as estimates — your actual increase depends on your own insurer’s rules.

- 0 demerit points (1–15 km/h over): approximately $510–$1,200 over three years (a 10–20% increase)

- 3 demerit points (16–29 km/h over): approximately $1,785–$4,335 over three years (treated as a major conviction by most insurers). This is the most common range for speeding tickets.

- 4 demerit points (30–49 km/h over): approximately $1,785–$4,335 over three years (major conviction for most insurers)

- 6 demerit points (50+ km/h over / stunt driving): approximately $7,650–$9,027+, or possible policy cancellation (a 150%+ increase)

- Two minor convictions: approximately $1,070–$1,925 cumulative over three years (a 21–32% cumulative increase)

What These Numbers Mean in Real Dollars

If you’re paying $2,000 per year for insurance and receive a 3–4 demerit conviction, that could mean an additional $595–$1,445 per year. Over three years, that’s roughly $1,785–$4,335 in extra insurance costs. Over six years (common for more serious convictions), it could reach $3,570–$8,670.

Put differently: a $150 speeding fine can quietly become a $1,900+ total cost once you add the insurance impact — and that’s before factoring in lost clean-record discounts. For a fuller breakdown of how points and premiums interact, see our guide on demerit points vs. insurance in Ontario.

What Factors Affect Your Specific Increase?

Insurance companies use multiple factors to calculate your post-conviction rate:

- Your age and driving experience. Younger and less-experienced drivers typically see higher percentage increases because they’re already in higher-risk categories. A young driver paying $4,000–$7,000 annually could see that jump toward $5,785–$11,335 after a major conviction.

- Your prior record. A first conviction on an otherwise clean record may have a smaller impact than a second or third. Drivers with existing convictions may see larger increases — or face non-renewal.

- The specific speed of conviction. Insurers distinguish between speeds. Being convicted at 17 over may be viewed differently than 28 over, even though both carry 3 demerit points.

- Your insurer’s specific policies. Different companies weight convictions differently. Some may be more forgiving of first offences; others may not.

How Long Does the Increase Last?

Most minor speeding convictions affect your insurance for three years. More serious convictions can extend to six years or longer, and some insurers look back even further when assessing new applications. This extended window is why the true cost of a speeding ticket is so much higher than the fine — that three-to-six-year premium increase is where the real money adds up. For more on the record side of this, read how long a speeding ticket stays on your record in Ontario.

The Clean-Record Discount Factor

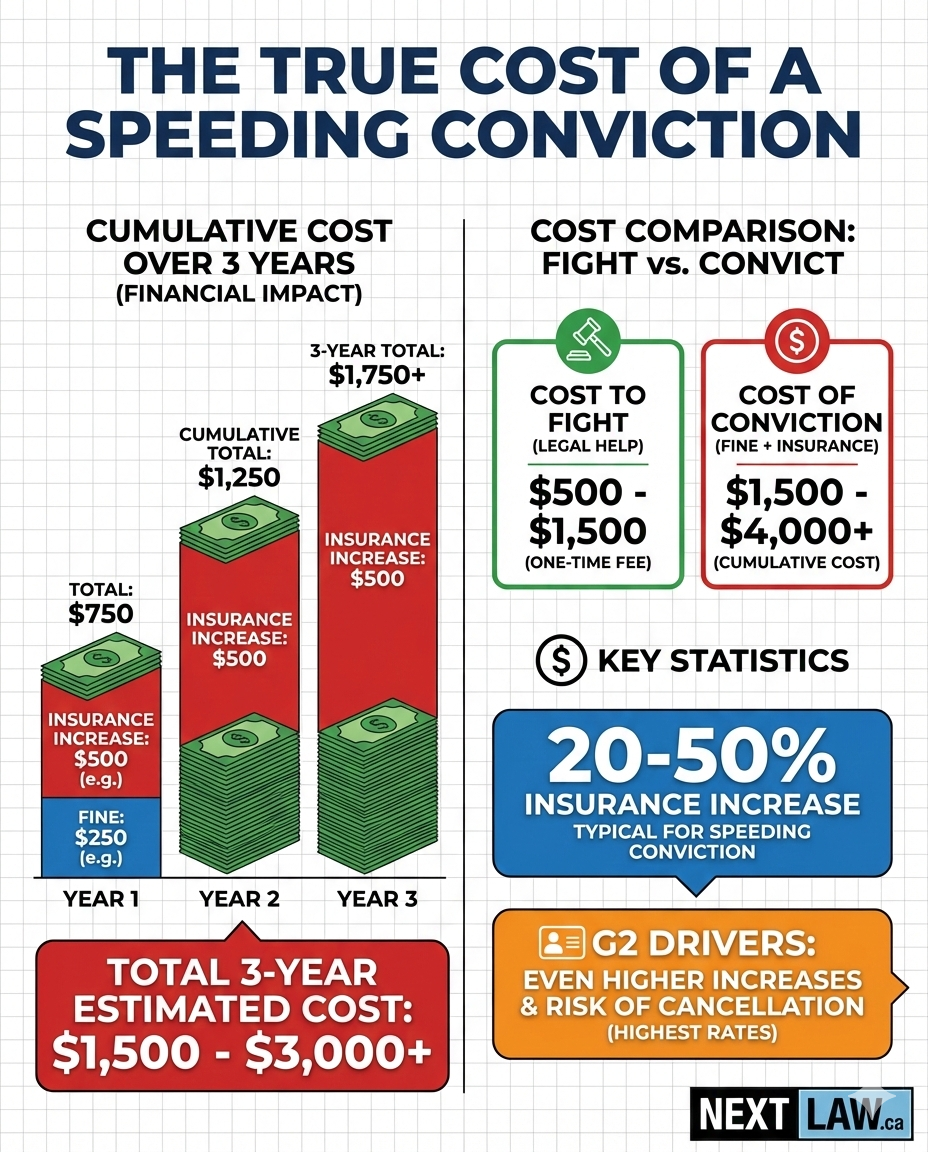

Many drivers don’t realize they’re currently receiving a “clean record” or “good driver” discount. A speeding conviction doesn’t just add to your rate — it can also eliminate this discount, creating a double impact. Losing a 10–15% good-driver discount on top of a 20–25% conviction increase could nearly double your premium. Protecting a clean-record discount is often worth more than the cost of fighting a ticket.

Can You Avoid the Insurance Increase?

The only way to completely avoid an insurance increase is to avoid the conviction. That usually means fighting your ticket and achieving a dismissal or withdrawal. Negotiating a reduced speed through early resolution may reduce the increase somewhat, but it typically doesn’t eliminate it — as long as there’s a conviction on your record, insurers will see it and rate accordingly.

NextLaw’s Sustained Pressure Strategy

Rather than taking the first resolution deal offered early, we opt for trial — not because we want a trial, but because the court rarely does. We request disclosure repeatedly, creating system friction. Pressure accumulates. At the trial date, there’s a small chance the officer doesn’t show (an immediate win); if the officer does show, we negotiate from a position of strength because the prosecutor wants to clear the case. It’s a named, deliberate approach — and it’s the kind of strategy most firms don’t walk you through on a first call. Here’s what actually happens at a speeding ticket trial in Ontario.

The 2026 Insurance Reform Context

Ontario’s 2026 auto insurance reforms have made insurers more aggressive about rating traffic convictions. The shift toward a “First Payer” model means insurers are now the primary payer in more claim scenarios. Speeding convictions can also affect your eligibility for enhanced Statutory Accident Benefits (SABS) coverage options, including Income Replacement Benefits and caregiver benefits. In other words, paying a ticket without contesting it may not just raise your premiums — it could reduce the coverage available to you when you need it most.

Making the Math Work for Your Decision

When deciding whether to fight your ticket, compare the cost of fighting against the insurance impact of a conviction. For most drivers, the math tends to favour fighting — the insurance savings from avoiding a conviction often exceed the cost of professional representation. Not every ticket is worth fighting, but every ticket is worth checking.

Frequently Asked Questions

How much does a speeding ticket raise insurance in Ontario?

A speeding conviction can raise insurance by roughly 10–20% for a minor (0-point) ticket and 20–30% or more for a major (3–4 point) conviction. For a typical driver, that often works out to somewhere between $510 and $4,335 in extra premium over three years, depending on the insurer, your record, and the speed. These are estimates — only your insurer can calculate your exact rate.

How long does a speeding ticket affect your insurance in Ontario?

Most minor speeding convictions affect insurance for three years from the conviction date. More serious convictions can stay relevant for six years or longer, and some insurers look back further when you apply for a new policy.

Does paying a speeding ticket make my insurance go up?

Yes. Paying a ticket is a guilty plea and creates a conviction on your record, which is exactly what insurers rate against. Paying is often the most expensive option once the insurance impact is included, because it guarantees the conviction.

Can I avoid the insurance increase after a speeding ticket?

The only way to fully avoid the increase is to avoid the conviction — typically by fighting the ticket and getting it dismissed or withdrawn. A reduction to a lower speed can lessen the impact but usually won’t remove it entirely.

Is it worth fighting a speeding ticket to protect insurance?

For many drivers, yes — because the potential insurance savings over three years can far exceed the cost of representation. The right answer depends on your specific ticket, so it’s worth having it reviewed before you decide.

Real Speeding Ticket Result

“I was charged with speeding ticket 67 over the limit on a G2 license. They got it down to 29 and no suspension. Happy with the outcome.” — Vijay Dhanda, NextLaw client (verified 5-star Google review #617)

Talk to a Speeding Ticket Law Firm

NextLaw is a law firm that focuses on fighting Ontario speeding tickets to protect your insurance. If you’d like to know what your ticket could really cost — and whether it’s worth fighting — a free call takes about 15 minutes and gives you clarity on your options. See why 825+ Ontario drivers have left NextLaw five-star reviews. Book a free call with NextLaw or explore our free tools to see what a conviction could mean for you.

About this estimate. Figures above are projections based on Ontario insurance industry data. Your actual premium change depends on your insurer’s proprietary rules, your policy, your driving record, and other personal factors. NextLaw is a law firm, not an insurance broker.

This article is provided for informational purposes only and is not legal advice. Every case presents unique circumstances, and outcomes depend on the specific facts and proper legal representation.